Consumer Funds & Property

200-12-DD & 604-01-DD

The Financial Plan

Every consumer will have a financial plan in his or her single plan.

This plan is like a blueprint of how a particular consumer's funds are to be managed.

The plan will state to what extent consumers are able to recognize money and manage their own funds. It will also state how much assistance a person needs in order to complete transactions .

Financial Plans

Financial plans will:

- Identify a consumer's financial ability, skills and needs.

- Establish a weekly spending allowance; a specific amount, not a range.

- Serve as a planning/management tool.

- Pay attention to long range financial planning, as well as routine monthly spending.

Financial Plans

Financial plans will also:

- Include a budget with annual income and expenses. This should include...

- All sources of known or anticipated income and all major categories of expenses. (Amounts should be estimated, and the budget must balance.)

- Fees for which the consumer is responsible.

- The amount that may be kept in cash and the method for getting cash.

Special Circumstances

Some special circumstances that should be addressed in the financial plan include:

- Provider is not representative payee for the consumer.

- More than $50 cash on hand for a consumer.

- Any exception to bank account guidelines.

- Sharing costs with other consumers.

Other Special Circumstances

Other special circumstances include:

- Any funds received which will not be deposited (e.g., holding some portion of a paycheck out in cash, rather than depositing the full paycheck.).

- Support for any use of a consumer's funds to pay for staff expenses. This should be done only on a case by case basis. There should never be a blanket "OK" to use a consumer's funds to pay for staff expenses.

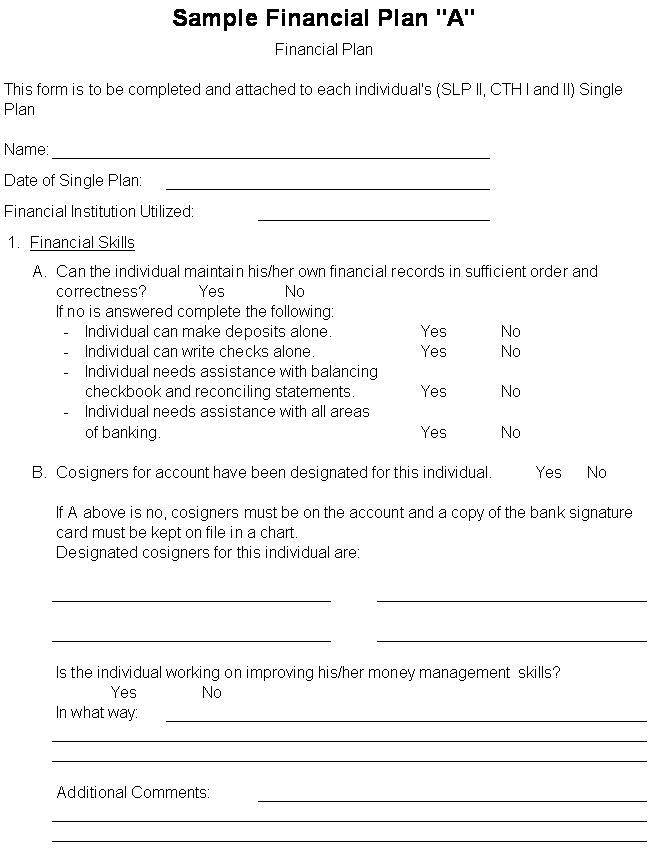

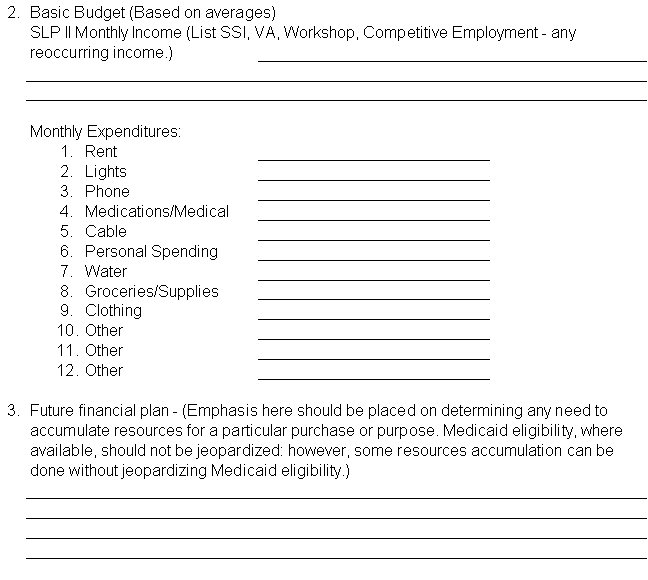

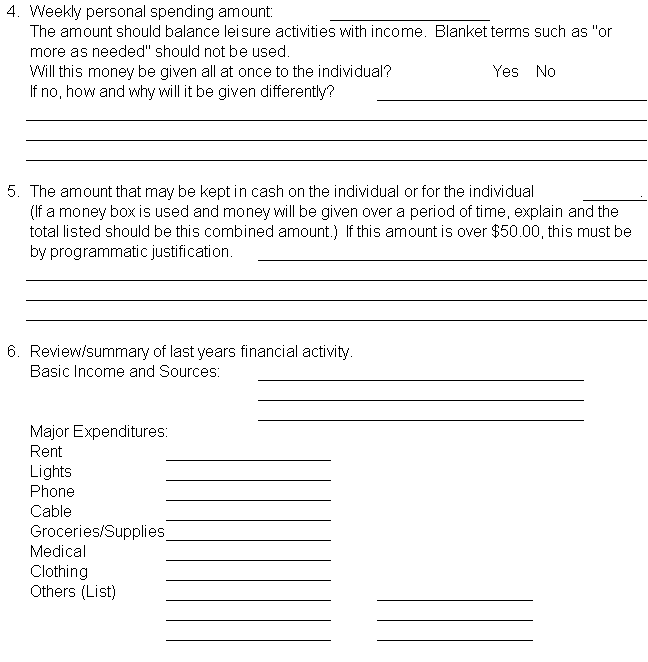

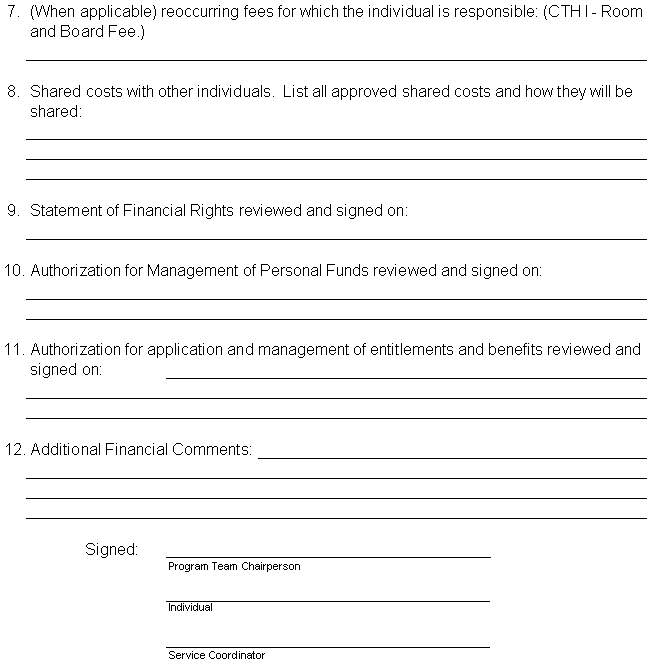

Sample Financial Plan

Sample Financial Plan

Sample Financial Plan

Sample Financial Plan

Sample Financial Plan

Set Up Bank Accounts

Set up a bank account for each consumer:

- The account may be a checking or savings account.

- The account must be separate from any provider account.

- Joint accounts with staff members are not allowed.

Consumer Bank Accounts

Consumer bank accounts:

- The account will be identified with the consumer's name, or will indicate that it is for the benefit of the consumer.

- John D. Baggodonuts.

- Sally Q. Caregiver, representative payee for John D. Baggodonuts.

- XYZ DSN Board for John D. Baggodonuts.

- A copy of the bank signature card will be kept in the consumer's file.

Consumer Bank Accounts

Consumer bank accounts:

- Co-signatures on checks are required.

- Consumers pay bank check and service charges.

- In many cases banks will waive check and/or service charges. Providers should work with area banks to find the best deal.

- Consumers must have reasonable access to their money.

Collective Accounts

Collective accounts are allowed with SCDDSN approval.

- Complete sub-account records are required.

- No fees are charged to consumers.

- Consumers should earn interest.

- Provider needs to show that the collective account would not be detrimental to the consumer and will be beneficial to the consumer.

How to keep a consumer's checkbook

Transactions

Receipt of funds:

- All monies must be deposited into his or her account unless otherwise specified in the financial plan included with the consumer's Single Plan/IPP.

- Deposits must be made within five business days of receipt.

- Do not withhold cash from deposit. (For cash needs, write a check to the individual from his or her account.)

- Unearned income (SSA, SSI, VA, etc.) should be on direct deposit.

- Record all deposits in check register at the time of deposit.

Transactions

Payments:

- A check should be written from the consumer's account for each week's spending money. (The check will be made payable to the consumer, and "weekly spending" noted both on the check and in the check register.)

- Never write a check to cash.

- Must make all major purchases ($50 or more) by check.

- Retain receipts of purchases except for incidental items of a non-permanent nature (snacks, movie tickets, etc.) Write the consumer's name and the check number on the receipt.

Transactions

Payments:

- Write no checks to staff without receipts for purchases. (Another staff should note on each receipt that the items were received by the consumer).

- Pay all provider fees by check.

- Co-sign all checks in accordance with the Single Plan.

- Record all checks in the checkbook register at the time the check is written.

Check Register

How to keep a check register:

- Make entries using black or blue ink only (no pencil, gel pens or erasable ink).

- Never use white out!

- Make the entry in the check register at the time the check is written or the deposit is made.

- Always keep a running balance (cash on hand) in the check register (this prevents you from bouncing a check).

Check Register

How to keep a check register:

- When you make a mistake in the check register — line through it and make the correct entry on the next available line in the register.

- If a check needs to be voided, write "void" across the face of the check and cut off the signature portion of the check. Also make an entry in the check register stating that the check was voided. Retain the voided check on file with the bank statements.

Reconciliations

Bank reconciliation of consumer accounts:

- Reconciliations will be completed within 10 business days of receipt.

- Reconciliations will be done by a staff member not authorized to co-sign on the checks.

- Accounts must be reconciled within five dollars ($5).

- Reconciliations must be documented. The reconciler should sign or initial and date the check register.

Reconciliations

Bank reconciliation of consumer accounts (cont.):

- Follow up on any accounts not reconciled within five dollars.

- Notify facility/program director, consumer's service coordinator/QMRP and the Executive Director.

- If the problem is still unresolved after five additional working days, the Executive Director should notify district office.

Reconciliations

Reconciling collective bank accounts:

- Reconciliation will be completed within 15 days after month's end.

- Reconciliation of collective accounts will be done by provider staff not authorized to receive or disburse any funds contained in the collective account.

- Account must be reconciled with fifty dollars.

- Reconciliation will be made between the account as a whole and the bank where the funds are on deposit.

Reconciliations

Reconciling collective accounts (cont.):

- Reconciliation must document that the consumer sub-account balances agree to the total collective account balance.

- Reconciliations must be documented.

- Follow up any problems with the Executive Director.

- The Executive Director will follow the guidelines for reporting unresolved problems with consumer accounts.

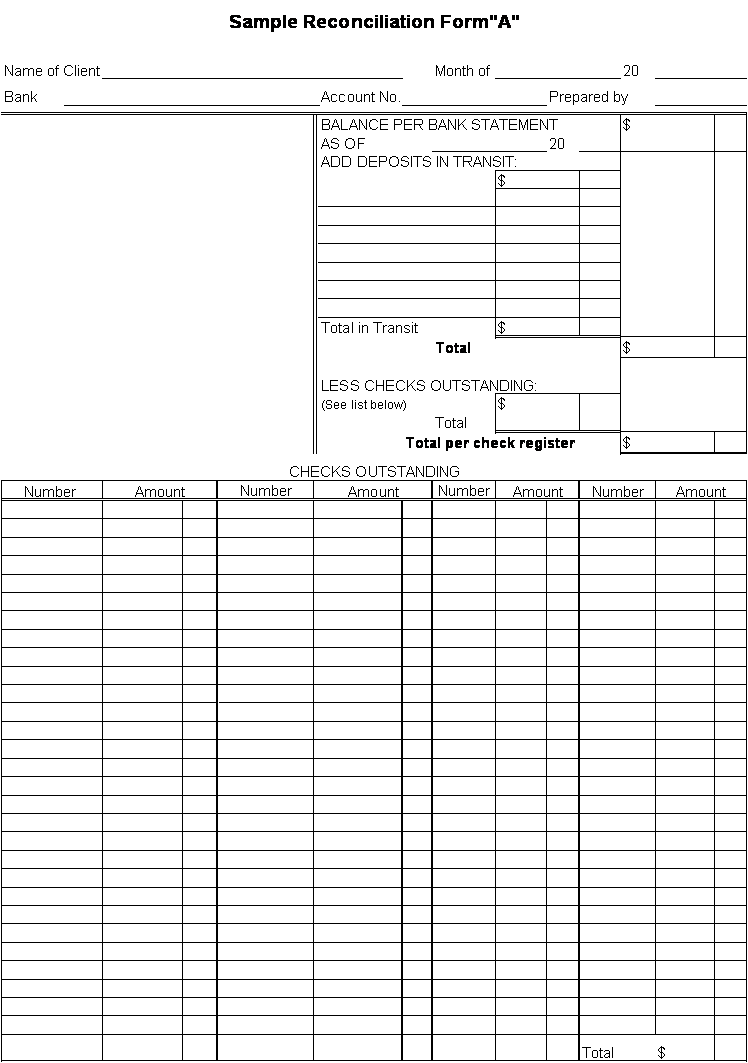

Reconciliation Form A

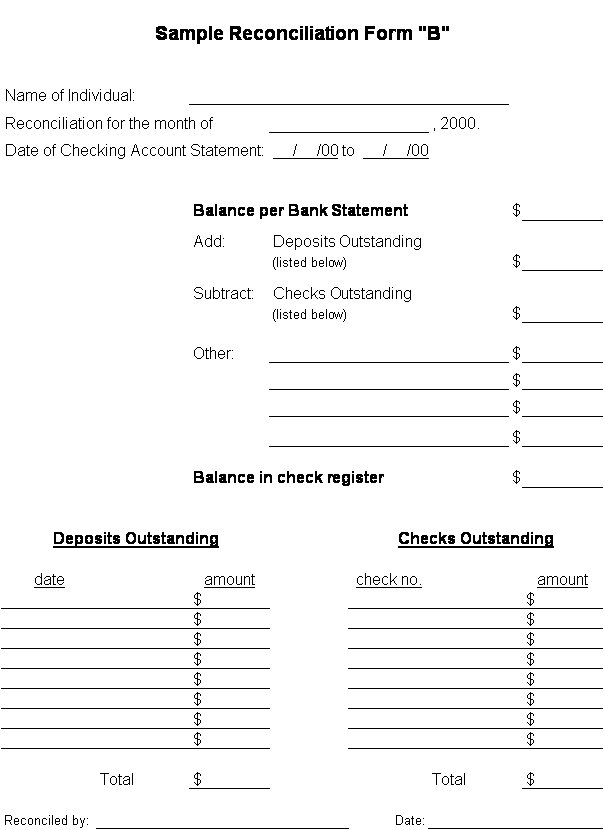

Reconciliation Form B

Sample Statement

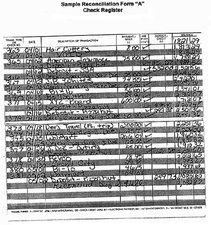

Sample Register

Sample Reconciliation

Sample Statement

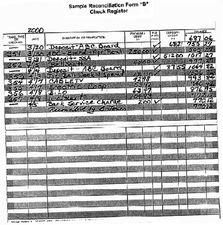

Sample Register

Sample Reconciliation

When cash

is kept in the homes

Cash on Hand

Rules for cash on hand at homes:

- Maximum cash on hand for each consumer will be stated in his/her single plan.

- A consumer's maximum cash on hand cannot exceed $50 without programmatic justification.

- Cash on hand includes both cash at the residence and cash in a consumer's possession.

- Cash on hand is not the same as a weekly spending allowance.

Cash on Hand

Rules for cash on hand at homes (cont.):

- Generally, cash on hand results from cashing weekly spending allowance checks. If weekly spending allowances are appropriately set, cash on hand should not exceed the limit.

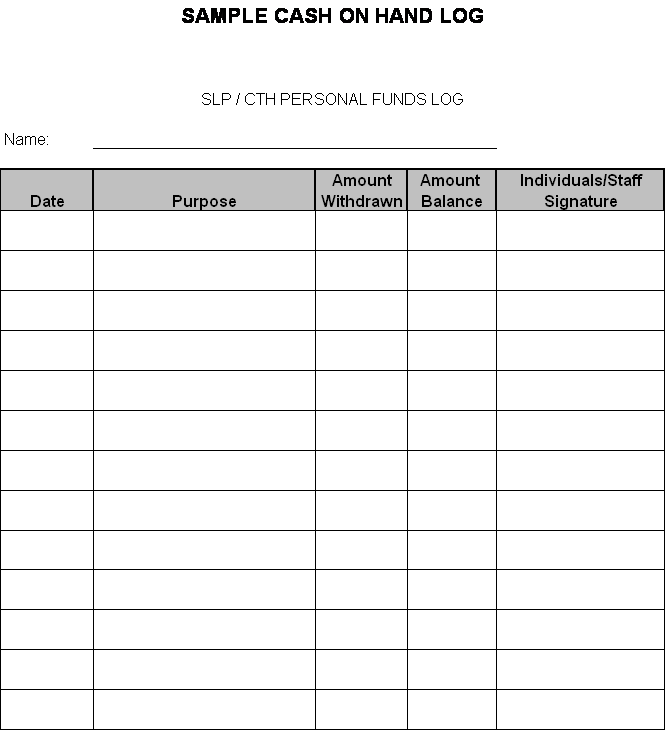

- Records must be kept for cash held on behalf of a consumer.

- Cash-on-hand records must be kept separate from the actual cash.

Cash on Hand

Rules for cash on hand at homes (cont.):

- Cash must be secured at all times and access limited to minimum number of staff.

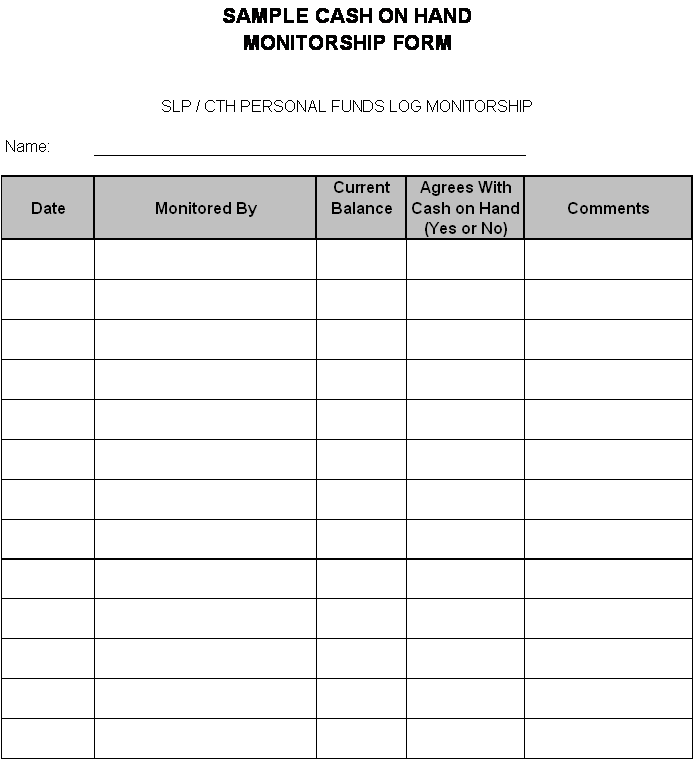

- Counts of the cash should be performed at least monthly by staff who do not hold cash or keep the records.

- Counts should be documented in the cash record. Person performing the cash count should sign or initial and date the cash record.

Cash on hand log

Monitorship form

Maintaining Records

Maintaining records:

- Original (not photocopy) receipts are required for all purchases made on behalf of a consumer.

- Receipts do not need to be kept for items of a non-permanent nature (snacks, movie tickets, etc.) or items that are not normally receipted unless the purchase was made by someone on behalf of the consumer.

- Keep all receipts with the monthly bank statement.

- Keep validated deposit tickets with the monthly bank statement.

- Keep earned income paycheck stubs with the monthly bank statement.

Maintaining Records

Maintaining records (cont.):

- Keep canceled checks with the monthly bank statement.

- Keep a copy of the bank signature card in the individual's file at the home/apartment.

- Keep bank statements, bank reconciliations, cash-on-hand records, and all supporting documents on file for six years.

- Keep other information that would be useful, including information presented to service coordinator/social services worker for review.

Report to Consumer

Reporting to the consumer:

- Give the consumer a report of his/her financial activity at least quarterly.

- The report should cover all income and expenditures by major categories and account balance(s).

- The report may be used as an information source for financial planning and monitoring.

- The report must be documented.

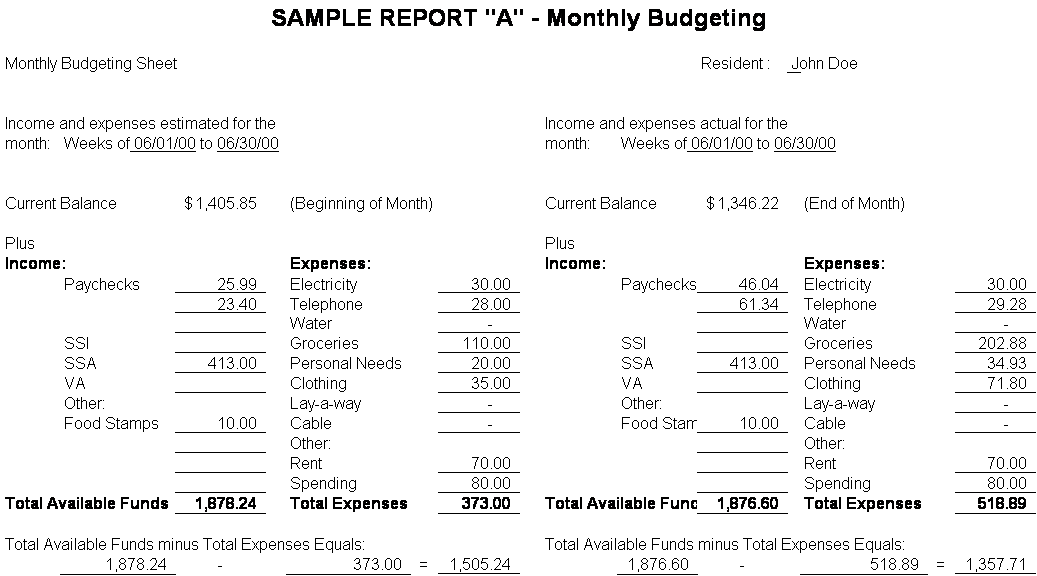

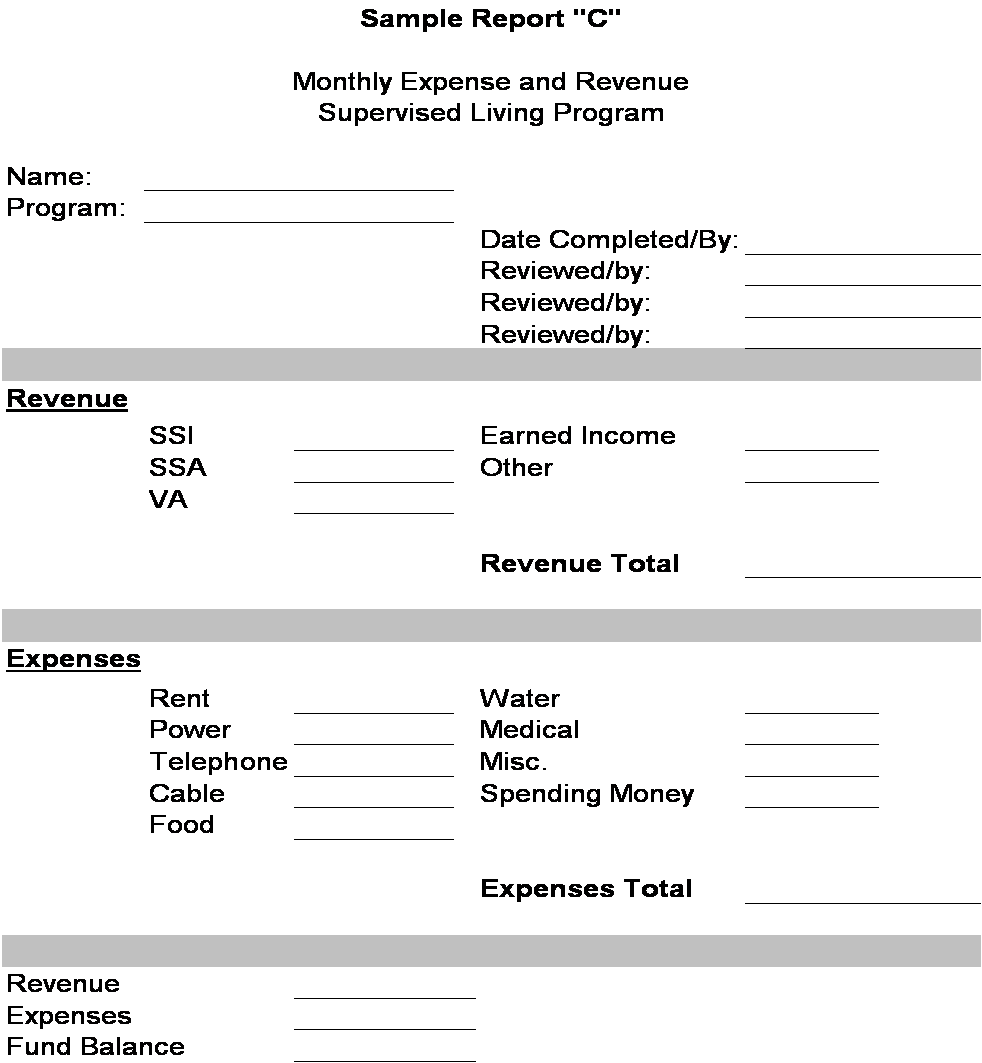

Monthly Budget

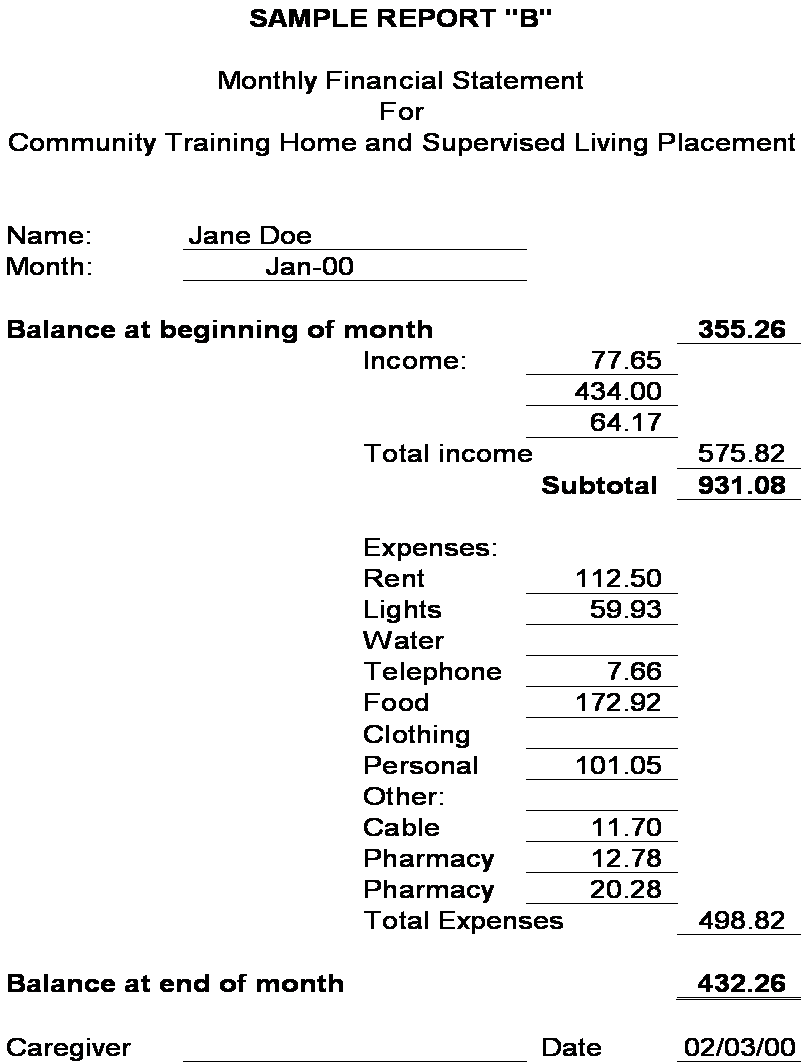

Monthly Financial

Expense & Revenue

Transfer or Discharge

Transfer or discharge of a consumer:

- Within 5 days send the most current statement of consumer's financial position to his/her new residence.

- Within 5 days, send a check for the available balance in the consumer's account to his/her new residence.

- Available balance is the current account balance less expected obligations (bills or checks not yet paid).

- After 60 days, send a check for the balance, if any, in the consumer's account to the new residence. All outstanding bills should be resolved by this time.

- Close the consumer's account.

Consumer Death

Death of a consumer:

- Within 10 days, notify the probate judge and other interested parties.

- Notification should include the following information:

- A complete listing of the deceased person's financial assets and obligations, including fees owed to the provider.

- The name and address of the parent, guardian or next of kin.

- The name and address of the executor/executrix, if known.

- A request for legal authorization for any disbursement of the consumer's funds.

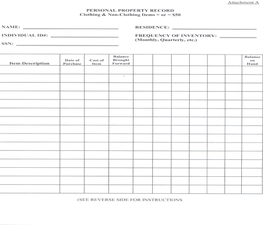

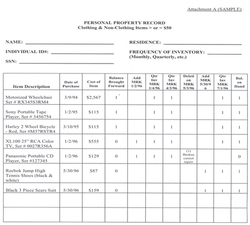

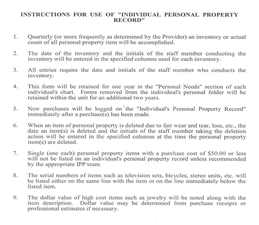

Consumer's Personal Property

Consumer Property

Rules for consumer's personal property:

- Marking of clothing - tags or indelible ink.

- Marking of non-clothing items - permanent engraving.

- Updating property records for additions & deletions currently.

Consumer Property

Rules for consumer's personal property (cont.):

- Quarterly inventories, not yearly.

- Large ticket items on property records ($50 or more).

- Serial and/or model numbers for appropriate items.

- Dollar value for large ticket items from receipts - insurance & theft purposes.

Property Record

Property Record

Property Record

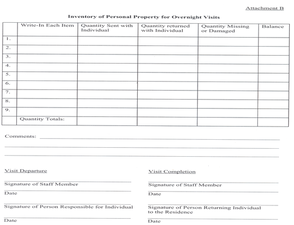

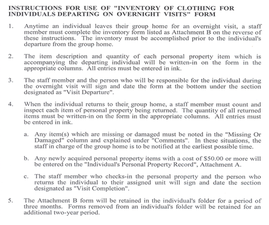

Overnight Record

Overnight Record

Thank You!

The next page will begin the competency quiz. Be prepared to enter your name and your e-mail address. A score of 80% correct is required to receive credit for completion.

Click here to begin the competency quiz.

Oops!

Use the "page up" key to return to the previous page. Click on the link to complete the competency quiz.

/